With the exception of those living completely off the grid, or people with no bank account, store accounts or any type of credit account, all South Africans have an extensive and detailed credit report that is registered with several companies known as credit bureaus.

As you conduct your accounts or apply for new credit, the reports are updated with both positive and negative information. When you wish to apply for credit, most companies will request a report from one or more of these bureaus to determine your credit worthiness. Their decision to grant you credit and the amount of the credit will be determined largely by the information on those reports. There are other considerations they will look at such as your affordability, for example, but the contents of the credit report will be their main source of information on which they base their decision.

What is a credit report?

A credit report is a historical analysis of your credit history. It contains detailed information regarding your past and current behavior with regards to any credit agreements you have currently or have had in the recent past.

The credit bureaus are private companies that collect data from all credit providers that you have transacted with (those that share the information, which is most of them). They then provide this information to credit grantors for a fee. In other words, if you apply for a loan, a bond, a credit card, vehicle finance, a store charge card, a hire-purchase agreement or any other form of credit, they company providing the credit will in all likelihood request and evaluate your credit report. They are also frequently used by companies or recruitment agencies when considering job applicants and they are often used by letting agents or landlords when evaluating prospective tenants.

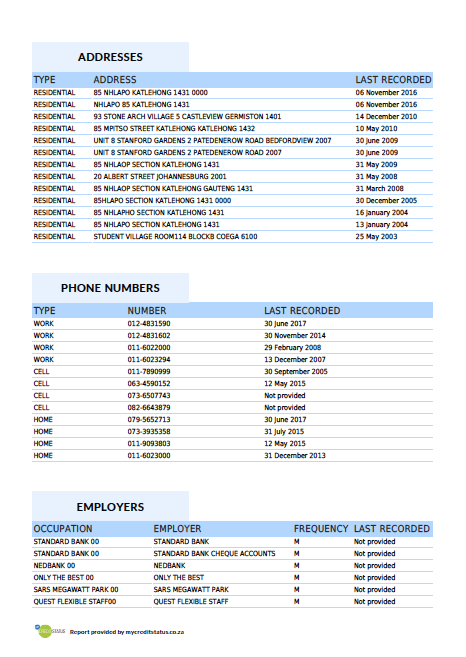

The report contains basic information such as your full name, address, ID number and employment details. It keeps historical information so will show not only your current address or employer but also previous information and the relevant time frames (ie. how long you have been at your current address or how long you have been with your place of employment.)

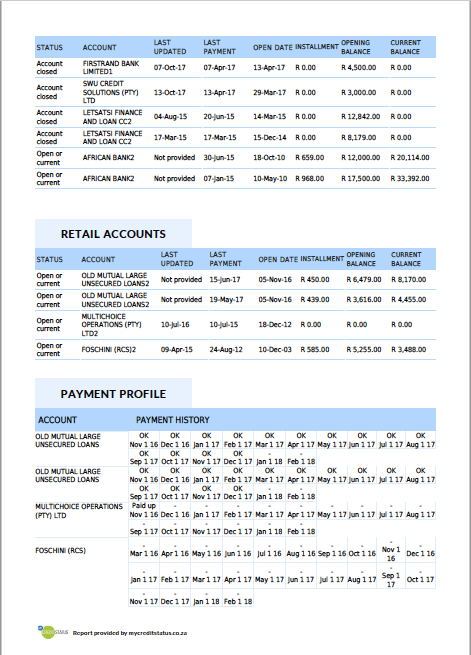

The next bit of information they track is your credit history which is a record of your payment habits and behaviour. This is normally in the form of a detailed record for each account, including the initial amount of credit, the monthly amount due, the date payment was received and the amount outstanding. If your accounts are in arrears or were in the recent past, it will show by how much and for how many days you were behind with payments.

When accounts go into arrears for a certain period, credit providers will post adverse feedback on the report, later, it will reflect as a default. If the debt is not paid for a long period of time and no arrangements are made to rectify the situation, the credit grantor will eventually go through a legal process and a judgment will be issued. All of this information will all appear on your credit report.

Credit reports will also reflect all inquiries made on your credit status. In other words, if you are, or have, applied at multiple institutions for credit, this will be visible on your report.

Obviously, accounts paid on time every month will also reflect this positive information on the same report.

Most credit bureaus apply a mathematical formula to data contained in the report, taking all positive and negative information into account and a credit score is generated. The credit score is the first and main thing that a potential credit grantor will look at when considering your application.

Who is allowed to view your credit report?

When you make an application for credit, you will generally sign a form giving the credit grantor permission to view your credit reports. The same applies to job applications, rental applications or any other instance in which a credit report is required. They may not view your report without your consent.

They will use this information to assess your risk profile and payment habits when deciding on whether or not to give you credit and if so, how much credit. They will take your affordability into consideration, based on the accounts and monthly commitments that reflect on your credit report. The state of your credit report will also, in many cases, determine the interest rate they charge you.

The importance of your credit report

As you can see from the above, it is in your best interests to maintain a healthy credit report. When you need to apply for credit or you wish to negotiate interest rates, a report in good standing will put you in a position of power and you will get preferential credit and interest rates.

Although fairly rare, sometimes incorrect information or even fraudulent activity finds its way on to you report which will have a negative effect on your ability to get credit and may even lead to other challenges.

It is therefore important that you are aware of your status with the credit bureaus and that you understand how the reports work.

Understanding your credit report

Now that you understand what the credit report is and how important it is, it is necessary to understand the health of your credit.

Just as you go to the dentist or doctor periodically, it is a good idea to do a “check-up” on your credit every so often.

The first step is to get a copy of your current credit report.

There are a number of bureaus registered in South Africa. The four main ones are:

Transunion Credit Bureau (Pty) Ltd (formerly ITC)

Experian South Africa (Pty) Ltd

Compuscan Information Technologies (PTY) Ltd

Xpert Decision Systems (Pty) Ltd – XDS

I would recommend approaching the first two at least and request a copy of your current credit report. This is normally a fairly simple, online process.

Once you have received it, read through and take note of all the information.

It is relatively self-explanatory.

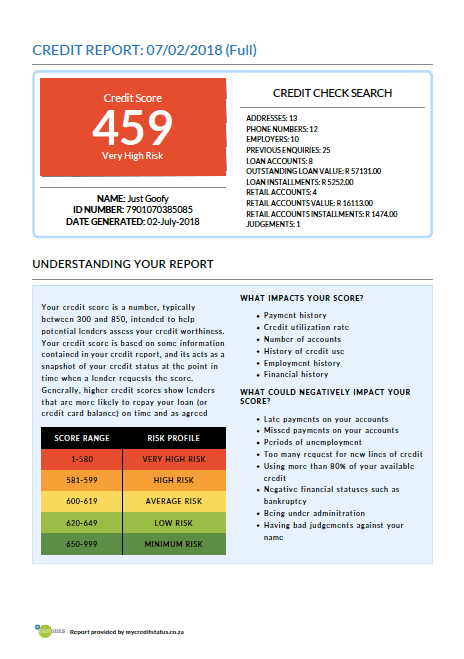

Below is an example of a typical credit report.

If there are any aspects that are unclear, the bureau has support staff that will be able to explain it to you. If there is incorrect information on the report, you can contact them to rectify it. If you have difficulty with this, see one of our later sections on how to dispute an error on your credit report.

Typical Credit Report Example:

Adverse Information

Defaults

Adverse No:

Adverse Date

Adverse Type

Written Off Date

Adverse Amount

Subscriber Name

AccountNumber

Supplier Contact Name

Supplier Contact Telephone Code

Supplier Contact Telephone Number

Supplier Details

Remarks

Judgements

Judgement No:

Judgement Date

Judgement Type

Defendant Name

Defendant Trade Style

Court Name

Claim Amount

Plaintiff Name

Attorney Name

Capture Date

Court Type

Case Number

Notices

Notice Date

Notice Type

Bond Percent

Court Name

Claim Amount

Plaintiff Name

Court Type

Case Number

Trace Alerts

Trace

Type

Subscriber

Name

Contact Name

Contact Phone

Comment

Debt Counselling

Debt Counselling Date

Debt Counselling Code

Printed Date: Wednesday, 20 November 2013 12:37 Page: 10/

Debt Counselling Description

Date Subscriber Contact Type

Consumer Activity

Previous Enquiries

This is a list of all companies and institutions that have made credit inquiries on you in the past

Final note

It is not advisable to bury your head in the sand and not want to look at your credit report. Making yourself aware of it and understanding it will assist you to improve it or, if it is already good, to keep it that way.

Fraud and errors do occur to which you might be oblivious and these could have a detrimental effect on your ability to raise credit. Take the time to obtain the reports at least once a year to assess the situation and take appropriate action where necessary.