As with anything, errors can creep into a credit report. It is important to inspect your credit report for errors in order to rectify them and have them removed.

There are a number of ways errors can appear on your credit report. Sadly, human error is one of the most common reasons for this. With improved technology, this is becoming less common but can still occur. This can happen at either the credit grantor’s side or at the bureau itself.

Fraud or identity theft is another reason for information appearing on your credit report that has nothing to do with you. Sadly, this is rife in South Africa. Again, technology and improved security are slowly improving this situation but it is still a very real problem.

Sometimes it is a legitimate credit account that you had but the details have not been updated or amended.

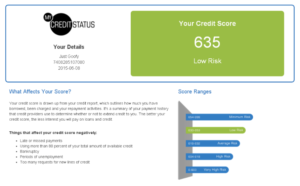

Check your credit report for errors

The first step is to do a credit score check and study it carefully to determine if there are any errors on the report.

The four most commonly used credit bureaus are:

– Transunion Credit Bureau (Pty) Ltd (formerly ITC)

– Experian South Africa (Pty) Ltd

– Compuscan Information Technologies (PTY) Ltd

– Xpert Decision Systems (Pty) Ltd – XDS

You can approach them directly or online to get a copy of your current report. If you would like more than one in a 12 month period there will be a charge.

There are also companies that will assist you, for a fee, with information on understanding your credit report and what action can be taken to improve it. They will assist in disputing incorrect information, again, for a fee. It can, however, be done yourself.

The Credit Bureaus want to have correct, accurate, and up-to-date information. More importantly, for the health of your own credit rating, you want to ensure it is accurate and error-free.

How to correct errors on your credit report

If you have identified any errors on your report, you need to dispute it with the bureau or bureaus in question.

Each bureau will have a system and procedure in place to deal with disputes. Generally, this can be done online for greater convenience. They also do have service agents that can assist you telephonically if you need guidance or advice.

You will have to explain the reason for the dispute and send them whatever proof or documentation you have to verify the correct information. They will launch an investigation into the disputed account.

Where they find that the information is not accurate or the data can no longer be verified, the bureau will amend or delete that record from your report.

If you have requested an investigation and after a period of 20 business days the dispute has not been resolved to your satisfaction, your next step is to contact the Credit Ombudsman and refer the dispute to them.

In cases where the information on the report is out of date and you wish to get it updated you can either approach the credit grantor and request that they update the information or you can ask the bureau to investigate the matter for you. It is important to follow up to ensure this is corrected.

If you notice inquiries from companies that have not been given permission to view your report, you would need to contact these companies to discover the reason for their inquiry. Often you may have given consent in the fine print of an application without realising it and/or, the name of the holding company may differ from the company you actually dealt with.

If you are not satisfied with the results of your investigation, you can request the bureau to investigate.

Identity Theft and Fraudulent Activity

If you are the victim of identity theft and someone has fraudulently used your ID and details to obtain credit, this can be a painful and frustrating process.

The first step is to approach the company that is reflecting the fraudulent information on your report. Request a copy of the credit agreement or application and report the matter to them.

Each company has their own policy and procedure but generally, you will have to put your complaint in writing and supply a copy of your ID. Often a police affidavit and sample signatures will be required.

The company will investigate and resolve the matter. Ensure you follow up. Again, if you do not get a resolution within a reasonable amount of time, take the matter up with the Credit Bureaus and lodge a dispute.

Report the matter to the police and open a case of fraud. Ensure you get a case number. It is also advisable to report the matter to the South African Fraud Prevention Service (SAFPS). You could also approach the Credit Information Ombudsman if the matter is not resolved to your satisfaction.

A final thought

If you do not check your report you will be blissfully unaware of the situation until you are declined for credit. This could cause major delays as well as much frustration. If you discover any errors, take the necessary steps t have them resolved. It is important to be proactive and follow-up, requesting proof that the issue has been correctly resolved.

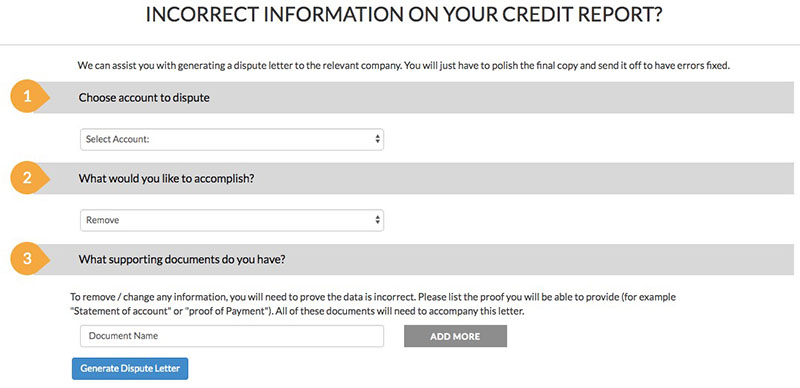

Getting a dispute letter from My Credit Status

If you are a monthly subscriber at My Credit Status then you will get access to our automatic dispute generator. This cutting edge tool will automatically draft a dispute letter for you with all the details of the dispute included. Here's how it works:

- Choose which account you want to dispute

- Choose if you want to remove, update or make other changes

- Enter the name of your supporting documents (if you have any)

- Click on "Generate dispute letter" and download the letter to your computer

Example Of The My Credit Status Dispute Generator: