We all know that the credit bureaus compile information on all credit transactions we are involved in and make these reports available to financial institutions and potential lenders when we are looking for credit, financing, or a loan.

We understand that they generate a score based on all this information and numerous other factors and this will impact our ability to access credit and very often, the rate of interest we will pay. Remember, with vehicle finance and particularly a home loan, even a 0.5% reduction in interest rate can make a significant difference. That is generally where the understanding ends and few people know what a good score is or what a bad score is.

Sadly, it is not like golf so the higher your credit score, the better. There are a number of bureaus in South Africa and they all work slightly differently but the end result of the score is relatively similar across the board.

Your score will help lenders understand your credit behaviour and determine whether you are a good or a bad risk. They can see your payment habits and make an informed decision when you request credit.

Some companies have very strict policies and knockout rules whereas others look at the report a bit more objectively. Either way, there is no avoiding the fact that a good score will help immensely while a low score will make your search for credit extremely challenging.

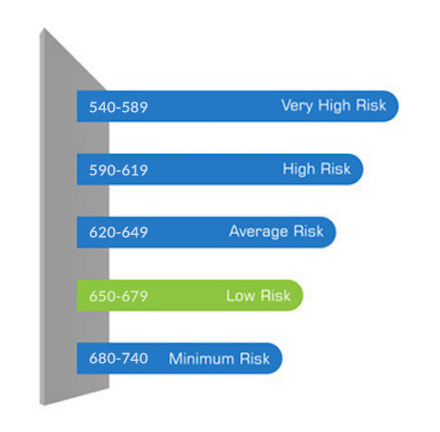

Credit scores in South Africa differ from bureau to bureau but generally start at 200 and go up to 705. Different financial institutions have different criteria and requirements, depending on the nature of the loan. Some loans are less of a risk than others.

As a general rule, this is how the scores are viewed:

540 – 589: Very High Risk

Anyone with a score below 589 will be viewed as very high risk with a high likelihood of not honouring the debt. As such, many companies will not consider them at all. Those that do will probably require a substantial deposit and/or collateral. They will also charge you more in terms of interest as a result of the increased risk they are accepting.

590 – 619: High Risk

This is a borderline area where lenders will tread very carefully as you will be seen as a high-risk client. Finance and credit will be extremely difficult but not impossible and when granted, will likely come with conditions and high-interest rates.

620 – 649 Average Risk

A score in this range is considered to be an average credit risk and you should not have much difficulty getting reasonable credit with fair interest rates if you do not have any judgements or listings behind your name.

650 – 679: Low Risk

At this level, things are looking up and the institution will look very favourably at your application. They will want to do business with you as you have proved you are a responsible user of credit and therefore pose a low risk to them. They are likely to offer you an attractive deal and you will have a strong negotiating position. Use it.

680 – 740: Minimum Risk

With scores this high, you are in a great position to negotiate finance and you should qualify for preferential terms and interest rates. Companies want to lend money to people with a score over 750 and will go out of their way to get your business.

As you can see, often just a few points can make a significant difference. Moving up a score bracket will be beneficial so make sure you do everything in your power to improve your score. An improvement of 10 or 20 points is not a major challenge with a bit of insight and effort.

There are obviously other factors that are taken into consideration but your credit score is one of the most important. Do everything in your power to maintain a good score or work damn hard to improve a bad score. With a low score, you will be going cap in hand to the lender whereas a higher score will put you in a position of strength and give you much greater power when negotiating the terms of the loan.